")

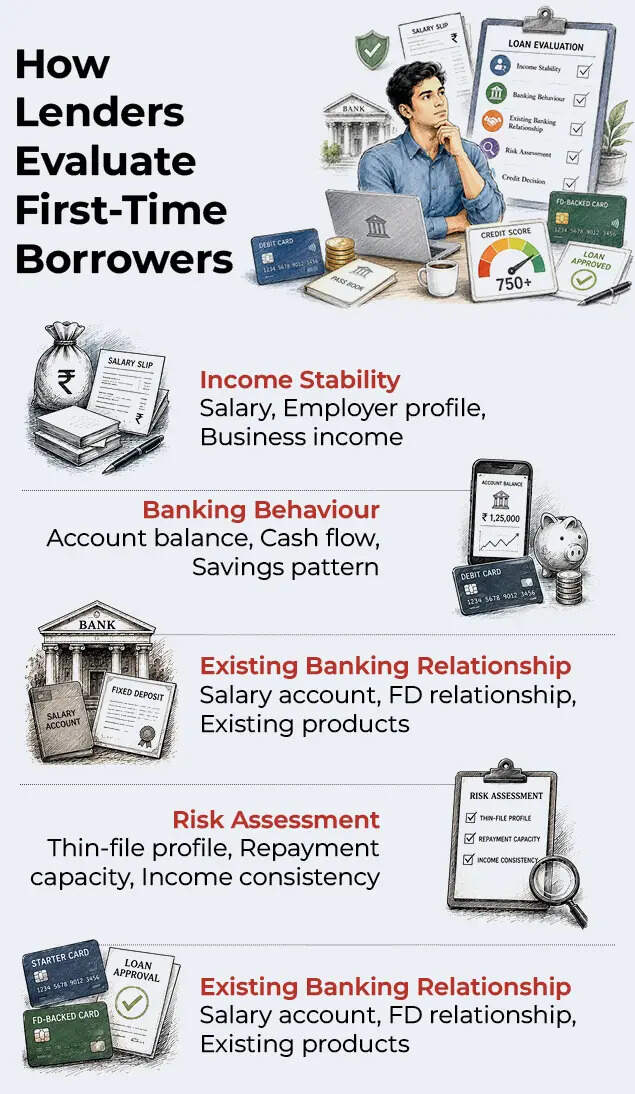

Getting your first loan or credit card can often be a challenge. Your lack of credit history makes it difficult for lenders to assess your creditworthiness, which essentially means banks and NBFCs have no historic data around your credit behaviour to judge whether you would be a reliable borrower and pay your EMIs and credit card dues on time. Due to this, many ‘new to credit’ customers are left with limited options.But understanding how lenders evaluate such applications can help you improve your chances of accessing formal credit. Existing Relationship with the BankNot having any credit accounts is a big disadvantage when looking to access new credit. But what can help is your existing relationship with banks, particularly those that hold your salary or savings account. Customers with a savings account or an FD with a lender for a long period have a good chance of getting a loan, even if they lack a formal credit history.Banks often extend loan offers to consumers who have salaried accounts with them, especially those working in large reputed organisations. This is because lenders can still map the lending risk based on how these borrowers have managed their existing products. Like, having a salary account with decent savings over time, signalling good financial discipline, helps. Thus, getting a loan or a credit card from a bank that holds your salary or savings account can be the best option. Job and Income StabilityLenders closely assess the job profile, the employer’s profile and the minimum monthly income of new-to-credit applicants when evaluating their loan eligibility.Applicants with a high and steady income are considered creditworthy by most lenders due to higher repayment capacity.Employer type is another crucial factor. Among these, salaried individuals employed with government organisations, reputed large private companies, MNCs and PSUs are most preferred. However, salaried employment alone may not guarantee easy access to credit. Applicants with frequent job switches, irregular salary credits or declining income trends may witness a stringent underwriting process. Lenders also evaluate the employer’s financial strength, industry outlook and salary consistency record while assessing the repayment risk. They conduct stricter underwriting assessments for employees working with financially-stressed companies, businesses experiencing operational instability or sectors undergoing prolonged slowdown.

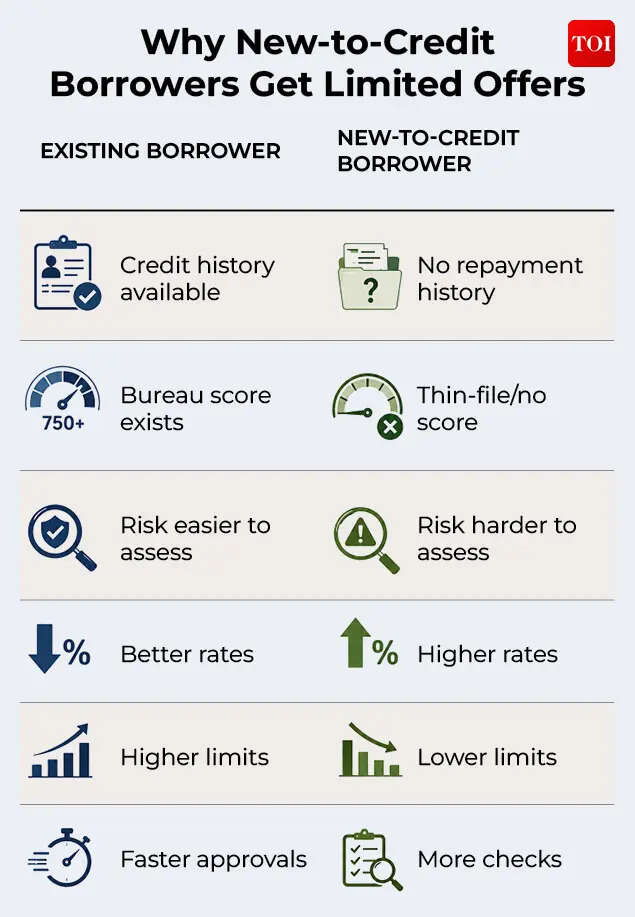

Self-employed applicants may find it difficult to get their loan applications approved due to the stricter scrutiny of income levels, and business cash flows that can fluctuate significantly depending on market conditions, business performance and sectoral risks. However, established businesses with a stable income, healthy cash flow management, strong banking behaviour and well-documented financial records provide more confidence to lenders that can translate into a better credit offer. Businesses demonstrating consistent turnover, profitability and financial discipline are often better positioned to negotiate improved loan terms, higher credit limits and relatively competitive interest rates.Bank Statements and Cash Flow BehaviourLenders usually analyse the bank statements of new-to-credit customers to assess their spending and saving habits. Maintaining healthy account balances and stable cash flows generally signals lower repayment risk to lenders. Lenders closely analyse GST filings, income tax returns, bank statements, profitability trends and business vintage to evaluate the creditworthiness of self-employed applicants. Prudent financial behaviour demonstrates discipline, which makes it easier for new-to-credit customers to avail loans. Challenges for Lenders in the Current Credit EcosystemLenders today operate in an ecosystem where access to credit is increasing rapidly, but it has also led to repayment stress in certain borrower segments. Where lenders can evaluate existing borrowers based on their repayment behaviour, there are limited options to assess NTC applicants, which leads to information asymmetry. Consumers today are entering the formal credit ecosystem much earlier than previous generations due to increasing digital adoption, online commerce and wider availability of small-ticket credit products. For financial inclusion, providing easy access to credit for first-time borrowers is crucial, but lenders also have to maintain strong underwriting standards for healthy books and long-term growth.The absence of past repayment behaviour for NTC applicants leaves lenders with only a few options, such as income stability, banking behaviour, etc., to assess their repayment capacity.However, over the last few years, the ecosystem has innovated to build new-age underwriting models that are able to offer credit to first-time borrowers, based on their financial behaviour. Transaction data, for instance, from payment and e-commerce platforms, is already being put to great use by lenders to build models that allow even new-to-credit consumers to get loans. New-to-Credit vs Poor Credit HistoryNew-to-credit borrowers are not the only borrowers that are perceived to be risky. Borrowers with a poor repayment track record, defaults and high delinquency pose a larger threat to lenders. While first-time borrowers may still be eligible for some loan offers, those with a poor credit score, especially caused by large unpaid dues, are unlikely to be eligible for even a single offer.

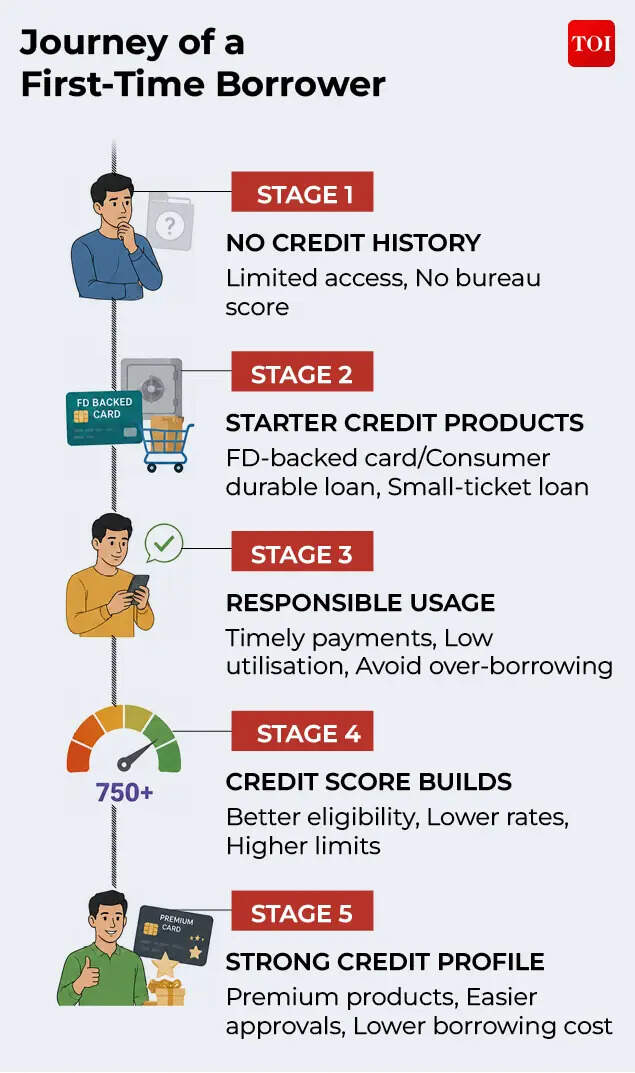

A disciplined credit behaviour from the very beginning is critical, as the initial stages of your credit history play a lasting and disproportionately important role in creating your creditworthiness. Responsible credit usage improves your creditworthiness and also helps build a credible financial identity.Even though existing borrowers with very good credit scores still remain the first priority for lenders, new-to-credit borrowers fare better than those with poor credit scores.How To Build Your Creditworthiness for the FutureThe first loan or credit card may not merely be a credit product for many borrowers but it marks the starting point of their formal credit identity. Since risk assessment is quite difficult for applicants with no credit history, one can take some steps to start building their credit history.

Opt for entry-level/FD-backed credit cards – Instead of approving a premium credit card, the provider usually offers an entry-level credit card with a lower limit or an FD-backed secured credit card. For those aiming to build their credit score, an FD-backed card is a strong, viable option.Addition of co-applicants – Lenders often encourage New to Credit borrowers to add a co-applicant, usually a family member, who has a strong credit score and stable income to cover the increased risk.Small-ticket loans – These loans carry low risk as the capital involved is very small. These products may involve relatively simpler eligibility assessments due to the lower ticket size, making it a convenient borrowing option for new-to-credit applicants. Repaying these loans on time can help build a strong credit score.To qualify for the best loan and credit card offers, a strong credit profile significantly improves access to better borrowing opportunities. Many borrowers availing credit for the first time may not understand the importance of building a healthy credit profile. Even minor repayment delays during the initial stages can have a significant impact on their credit profile and affect their creditworthiness. Staying aware and repaying dues with discipline can help build a strong credit profile.Some first-time borrowers make multiple loan or credit card applications for a single credit product. Applying for a credit product with multiple lenders can negatively affect a lender’s risk assessment, flagging serious concerns even at the start of the credit journey. Making timely repayments and keeping your credit utilisation low can help build a strong credit history over time. Consumer durable loans, if feasible, can also help build their credit history.For the credit industry, improving financial literacy among first-time borrowers is equally important as improving access to credit. Understanding how credit score, repayment behaviour and credit utilisation affect future borrowing opportunities can help new consumers make more informed financial decisions.A high credit score opens the door for credit offers at better terms and at a relatively lower cost of credit. Once your credit score starts building, monitor it periodically to maintain strong credit health. NTC consumers should view credit accessibility as a financial responsibility rather than just another borrowing opportunity.(The author, Santosh Agarwal is the CEO of Paisabazaar)

Leave a Reply